Just over a week after Turkish president Erdogan revealed a stunning (in its stupidity) “whatever it takes” scheme to stabilize the Turkish currency by pledging to make whole losses linked to inflation (shocking Turkey watchers everywhere because the “tactic” was too insane even by Erdogan standards) in hopes of halting the relentless collapse in the Turkish lira, a move which together with billions in illicit dollar sales by the central bank sparked the biggest surge in lira history just as it was about to fall into a hyperinflationary abyss, the honeymoon is now over and Turkey’s lira has fallen for a third day amid renewed demand for dollars even as the central bank continued to take unprecedented, if doomed, steps to support the currency.

The lira traded 7.5% lower at 12.67 per dollar as of 5:26pm in Istanbul, taking its 3-day move to almost 20% higher after enjoying a historic surge just a week ago amid a furious short squeeze. Even with the recent slide, the USDTRY is still down 24% from where it traded early last Monday, ahead of the unprecedented fireworks.

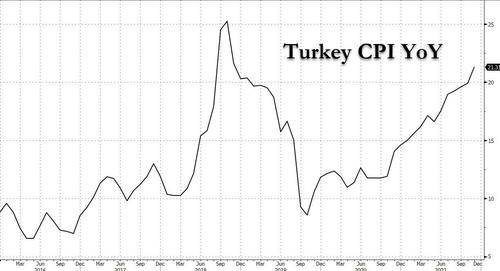

As a reminder, last week Erdogan introduced FX-linked deposit accounts aimed at protecting lira savings from the currency’s decline. The monetary authority published its annual policy text today, stating that inflation targeting will continue in 2022, while a 5% medium term inflation target is maintained. Of course, real inflation in Turkey is now well over 21%.

There’s more: telegraphing just how little actual FX reserves Turkey has (recall that the country is now exclusively reliant on FX swaps to manage the currency as its net FX reserves are massively negative), the central bank announced a fresh measure today aimed at boosting the currency, saying it would support conversion of saving accounts in banks in gold to holdings in lira. Similar to the insanity spouted last week, the central bank said it would make up for losses incurred by holders of lira deposits should the currency’s decline against gold exceed bank interest rates.

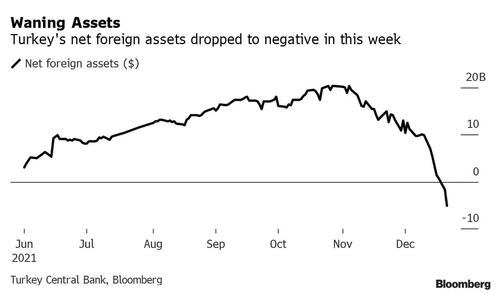

The step comes after the central bank had announced a similar support mechanism on Monday for deposits in foreign exchange converted into liras in an attempt to discourage savers from switching savings into dollars. The idea – to provide a government guarantee against FX losses on lira deposits, which is as ridiculous as it sounds as it merely shifts the risk to the government balance sheet – was also floated in the midst of the last currency crisis in 2018, but it was shelved at the time due to risks. This time the risks – which have already sent Turkey’s CDS blowing out – were seen as acceptable. Meanwhile, we also noted last week that in addition to the psychological “shock and awe” of the Erdogan loss-offset strategy, the central bank sold so much in hard assets, its net foreign assets plunged to negative last week, ensuring that another currency crisis was inevitable.

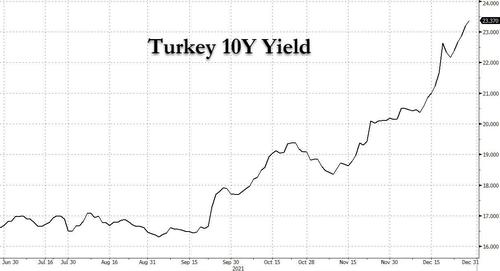

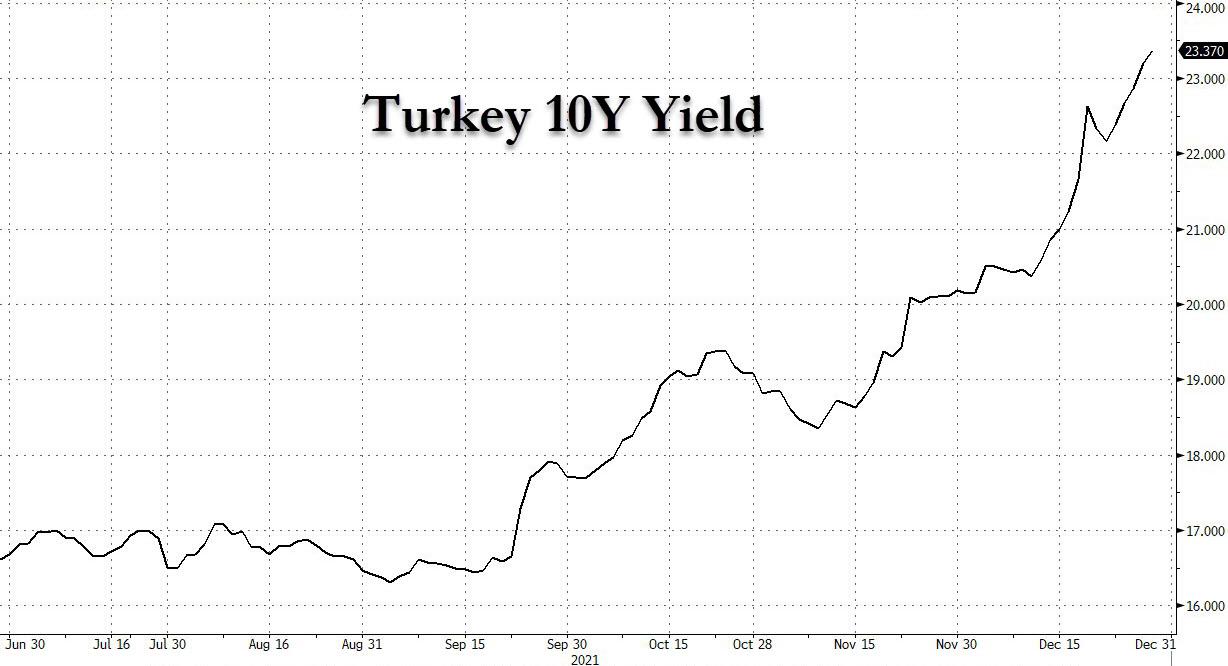

And sure enough, while the drop in the lira was guaranteed and as we said last week, just a matter of when not if, this time the drop in the Turkish currency is also dragging Turkey’s 10-year government bonds sharply lower…

… which today are yielding a record 24%, just as we warned would happen now that Erdogan has managed to launch the infamous “Doom loop” which plagued Europe for so long by linking weakness in FX to weakness in bonds, creating a procyclical nightmare for policymakers.

The only difference: the ECB was at least run by a competent former Goldmanite. Turkey, unfortunately, has no such luck.

Which is why when – not if – the lira selloff accelerates, it will immediately lead to higher yields, which in turn will lead to an even lower currency and so on until the entire economy implodes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}